Emerging Markets Mirror U.S with Tech, AI Dominance

EM Equities are powering forward despite the Iran war, but the gains are driven largely by tech companies fueled by the AI super cycle. Concentration risk is rising.

There’s a slew of good pieces out there on how emerging markets stocks are faring amid the Iran war. The picture is mixed, but the winners - think Taiwan, South Korea, Brazil - are winning big and powering the index to another strong start for 2026. The ishares MSCI Emerging Markets Index ETF (EEM) is up more than 19% on the year - after a strong 2025 that saw 33%+ gains on the index.

One theme that has emerged in a lot of the reporting focuses on rising concentration risk in emerging markets. Namely, Taiwan and South Korea lead the pack, and a handful of tech behemoths lead those markets. Think Samsung, SK Hynix, TSMC.

Barron’s has a good piece this week by Andrew Barry that compares two leading emerging market index funds, noting that the key performance differentiator comes down to two words: South Korea. Namely, one of the funds has heavy South Korea exposure and the other doesn’t.

In the battle between the two leading emerging market stock ETFs, iShares has the advantage. South Korea is making all the difference.

The $150 billion iShares Core MSCI Emerging Markets exchange-traded fund (ticker: IEMG) has significantly outperformed its chief rival, the $119 billion Vanguard FTSE Emerging Markets ETF (VWO) in 2026 and over the past 12 months. That’s because the iShares ETF has exposure to the hot Korean market, while the Vanguard fund doesn’t.

The iShares ETF, now trading around $78, has jumped 38% over the past year and 18% so far in 2026, while the Vanguard ETF, at about $58, has gained 22% in the past 12 months and 9% so far in 2026.

South Korea, one of the hottest stock markets in the world, accounts for the bulk of the disparity. The country’s semiconductor-led market has skyrocketed about 75% this year and nearly tripled over the past 12 months. The Korean market now accounts for about 20% of the iShares ETF, double its weighting of a year ago.

Another piece by Jared Mitovich in the Wall Street Journal from a couple of weeks ago explores this phenomenon of the tech-heavy emerging markets story. Some excerpts below.

Emerging Market Stocks Are Powering Past the War

The Wall Street Journal

A war that seemed primed to pummel emerging economies reliant on Middle East imports hasn’t done the same to their stock markets.

Investors feared that the energy shock would derail a big year for international stocks, particularly in the developing world. Instead, the MSCI Emerging Markets Index rebounded to new all-time high…

…One major driver: artificial intelligence. South Korea and Taiwan are home to key suppliers to the AI build-out in the U.S. and around the world. That includes Samsung and Taiwan Semiconductor Manufacturing, both of which have posted double-digit stock gains so far this year.

That has helped those markets offset the blow from rising energy prices. And analysts said some emerging-market economies, like Brazil, are better-poised to withstand the war’s disruptions as oil exporters less dependent on energy from the Middle East.

There’s a good quote in the piece by Sarah Ketterer, chief executive of Causeway Capital Management. She said: “People still mentally write off the emerging markets because ‘they’re ex-growth, because China is still the dominant market at 30%, and why bother when the U.S. is so good…But in the emerging markets [there] are some amazing growth stories.”

Ruchir Sharma wrote last month about what he called “a retro rally” in emerging markets. He also focused on the heavy concentration of AI super cycle stocks. He writes

At the height of the internet boom in 2000, Wall Street salespeople tried to add a digital lustre to emerging stock markets by rebranding them as ‘e-merging markets’. A quarter of a century later, amid the euphoria for AI, a similar story is unfolding.

The same tech stars, South Korea and Taiwan, are driving a kind of retro rally. Over the past year, these two nations accounted for 75 per cent of emerging market returns, and most of those gains came from just three stocks — all big makers of semiconductors. Korea and Taiwan have arguably sprung to the fore as the biggest beneficiaries of the global AI boom. Amid tight supply, AI-driven demand has driven up prices for semiconductors made by TSMC, Hynix and Samsung to record levels.

With America’s big tech companies on course to invest $700bn in AI capex this year, their free cash flow is disappearing, but their heavy spending is boosting the profitability of the three north Asian giants. Together their profits are on track to top those of Apple, Amazon and Alphabet combined.

Let me pause for a moment, and allow that fact to sink in:

“Together their profits are on track to top those of Apple, Amazon and Alphabet combined.”

We’re certainly entering new territory here with these three companies.

There’s more from Sharma below:

Samsung is expected to increase operating profit more than sixfold this year to around $185bn, surpassing every member of the “Mag Seven” American companies other than Nvidia. As a result, with a boost from large and avid populations of local retail investors, these markets have gone parabolic in recent months — as was the case in 1999-2000.

Much has changed in the intervening decades. While the leading creator of stock market indices, MSCI, still classifies South Korea and Taiwan as emerging markets, they are developed countries in every other way. They now have per capita incomes over $35,000, which is more typical of developed than developing nations.

…The recent surge has made this boom the most powerful of the past 10 global up cycles, with global semiconductor sales up more than 60 per cent over the past year. Investors are pushing the big north Asian chipmakers up the ranks of the world’s largest companies by market cap. TSMC is the most widely held stock, owned by 92 per cent of global equity funds. In comparison, Microsoft, the most widely owned US stock, is held by 84 per cent of those funds.

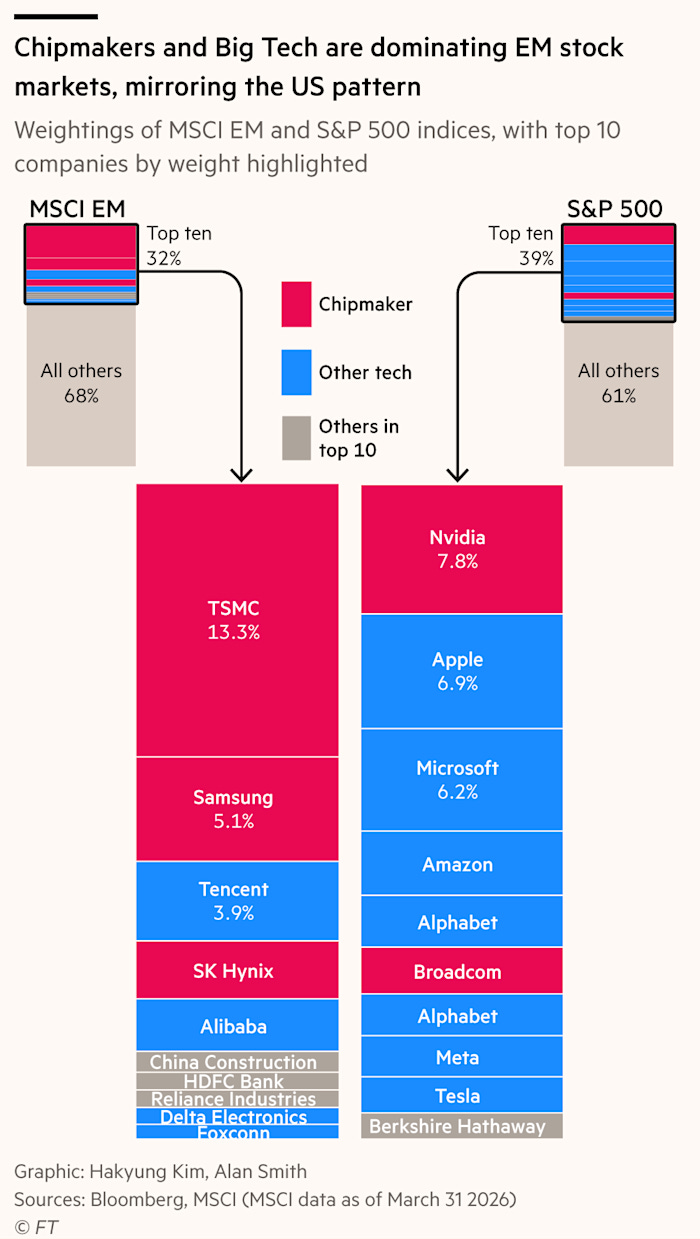

It’s no secret that mega tech stocks have been dominating — some would say distorting — the US market for years. Today, by some measures, emerging markets have grown even more concentrated than the US, with the leading five stocks accounting for a greater share of the index. While the top US stock (Nvidia) represents 8 per cent of the US index, the top EM stock (TSMC) accounts for a record 13 per cent of the EM index.

In fact, based on MSCI methodology, TSMC now constitutes a larger share of the MSCI EM index than all the stocks in India put together. It wasn’t supposed to happen this way. China was expected to be the second biggest beneficiary of the AI boom after the US. Instead, still struggling to figure out how to profit from AI, Chinese giants led by Alibaba and Tencent have been registering paltry stock price gains compared with their counterparts in South Korea and Taiwan.

The FT’s Hakyung Kim and Alan Smith created a great infographic that reflects this concentration risk:

Kim writes:

Historically, developed market investors have looked to emerging market stocks for diversification. In addition to providing exposure to different economies and (in some cases) lower valuations, emerging market assets provided exposure to sectors under-represented in developed world indices, such as energy and commodities.

Increasingly, however, emerging market indices have fallen into the same pattern as the US market — top-heavy and tech-oriented. The MSCI EM index has surged 14 per cent this year, more than double the S&P 500’s gains, as Asian chipmakers have powered higher. A decade ago, the entire IT sector accounted for less than 20 per cent of the benchmark MSCI EM index. Today, just three chipmakers — TSMC, Samsung and SK Hynix — account for 21 per cent of the index. This shift has also reduced the index’s geographic variety, leaving its fate highly dependent on the tech hubs of Taiwan, South Korea and China.

The dominance of tech in emerging market indices exposes them to the same bubble fears that loom over the US market. The indices will also change dramatically if, or when, South Korea and Taiwan get promoted to developed market status. Both countries have worked towards improving market accessibility to receive upgrades; for South Korea, the change could come as soon as sometime this year and take effect in 2027.

So, what does this all mean? Here’s my view:

Emerging markets are often sold to investors as a story of diversification that will give the investor exposure to different growth engines, commodities, demographics, and industrialization cycles far removed from Wall Street. But, in reality, the story looks familiar to US and advanced economy investors: concentration, mega-cap dominance, and a handful of AI-linked companies driving index performance.

That doesn’t mean the emerging markets story is broken. After all, the story is not only about stock markets. Brazil, India, Southeast Asia, Latin America and parts of the Middle East still represent some of the most dynamic growth stories in the world economy.

But investors should recognize that today’s “emerging markets” index investments are no longer simply a broad bet on the developing world. Increasingly, they are a highly concentrated wager on semiconductors, AI infrastructure, and the fortunes of a few global tech champions.

The irony is striking. As many investors are looking outside the United States to diversify away from America’s mega-cap tech concentration, they may be finding themselves right back in another version of the same trade, only this time through Taipei and Seoul instead of Silicon Valley.

“You don’t have to be great to start, but you have to start to be great.” — Zig Ziglar

“Do what you can, with what you have, where you are.” — Theodore Roosevelt